3 min read

5 Steps to Get Started with ESG Compliance

We all know how quickly the global business landscape is shifting to Environmental, Social, and Governance (ESG)...

![]()

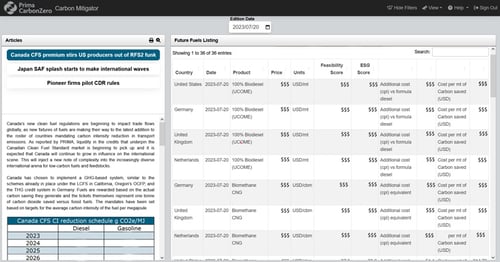

Prima CarbonZero is an intuitive platform that delivers comprehensive data and expertise. Designed for business leaders and analysts at organizations that produce, trade, and invest in low-carbon fuels and feedstocks.